All Categories

Featured

Table of Contents

Term Life Insurance is a type of life insurance coverage plan that covers the policyholder for a specific quantity of time, which is called the term. The term sizes vary according to what the individual chooses. Terms commonly vary from 10 to 30 years and increase in 5-year increments, giving degree term insurance coverage.

They usually give an amount of insurance coverage for much less than permanent types of life insurance policy. Like any plan, term life insurance has advantages and downsides depending on what will work best for you. The advantages of term life consist of cost and the capability to personalize your term size and insurance coverage amount based upon your requirements.

Relying on the kind of plan, term life can use repaired premiums for the whole term or life insurance coverage on degree terms. The fatality advantages can be repaired. Since it's a cost effective life insurance product and the repayments can stay the same, term life insurance policy plans are preferred with youths just beginning out, households and individuals that desire security for a particular amount of time.

*** Fees reflect policies in the Preferred Plus Price Course problems by American General 5 Stars My agent was extremely experienced and practical in the process. July 13, 2023 5 Stars I was satisfied that all my demands were satisfied quickly and skillfully by all the representatives I talked to.

What is Term Life Insurance Level Term and Why Choose It?

All paperwork was digitally finished with accessibility to downloading and install for individual documents upkeep. June 19, 2023 The endorsements/testimonials presented must not be interpreted as a referral to purchase, or an indication of the worth of any type of product or solution. The testimonies are actual Corebridge Direct customers who are not affiliated with Corebridge Direct and were not offered compensation.

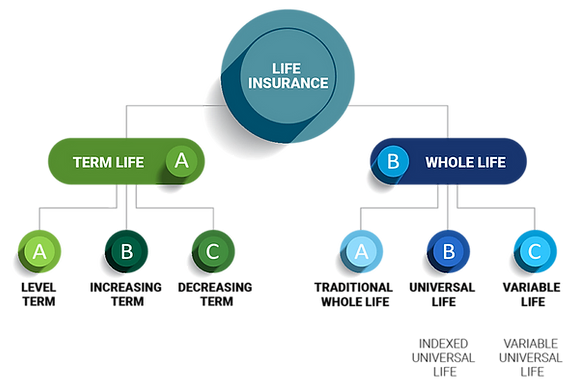

There are several kinds of term life insurance coverage policies. Rather than covering you for your entire life-span like whole life or global life policies, term life insurance policy just covers you for a designated time period. Plan terms generally vary from 10 to 30 years, although shorter and longer terms might be available.

If you want to maintain insurance coverage, a life insurance provider might supply you the choice to restore the plan for another term. If you included a return of costs motorcyclist to your plan, you would get some or all of the cash you paid in premiums if you have outlived your term.

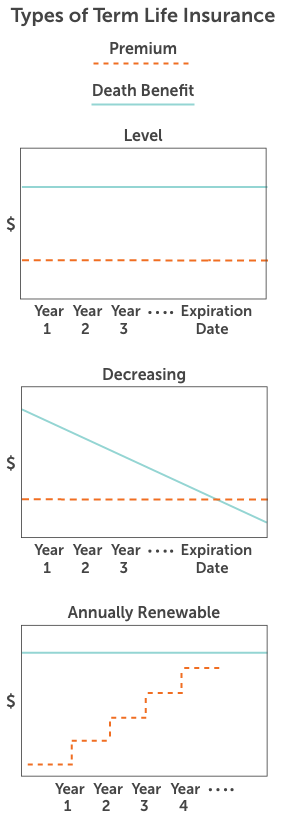

Level term life insurance policy might be the most effective choice for those who want coverage for a set duration of time and desire their costs to continue to be stable over the term. This may relate to consumers worried concerning the price of life insurance policy and those that do not intend to alter their survivor benefit.

That is because term policies are not ensured to pay out, while permanent plans are, supplied all costs are paid., where the death advantage reduces over time.

On the other side, you might have the ability to protect a more affordable life insurance policy rate if you open up the policy when you're younger. Comparable to advanced age, poor health can also make you a riskier (and a lot more costly) candidate for life insurance coverage. Nevertheless, if the problem is well-managed, you may still be able to find budget friendly insurance coverage.

What is a Level Term Life Insurance Meaning Policy?

Health and age are generally much extra impactful premium elements than gender., may lead you to pay even more for life insurance policy. Risky work, like home window cleaning or tree cutting, may additionally drive up your cost of life insurance.

The primary step is to establish what you require the policy for and what your spending plan is. Once you have a good idea of what you desire, you may intend to compare quotes and plan offerings from several business. Some firms use online pricing estimate forever insurance policy, but lots of need you to contact a representative over the phone or face to face.

1Term life insurance provides momentary defense for a critical duration of time and is usually less costly than permanent life insurance policy. 2Term conversion standards and restrictions, such as timing, might apply; for instance, there might be a ten-year conversion advantage for some items and a five-year conversion advantage for others.

3Rider Insured's Paid-Up Insurance Purchase Option in New York. There is a cost to exercise this biker. Not all participating policy proprietors are eligible for rewards.

Our term life alternatives consist of 10, 15, 20, 25, 30, 35, and 40-year plans. The most preferred type is level term, suggesting your payment (costs) and payment (death advantage) remains level, or the very same, till the end of the term duration. Decreasing term life insurance. This is the most uncomplicated of life insurance policy options and requires extremely little maintenance for policy owners

For instance, you could give 50% to your spouse and divided the remainder among your grownup kids, a moms and dad, a close friend, or perhaps a charity. * In some circumstances the death advantage might not be tax-free, learn when life insurance policy is taxable.

What is What Is Direct Term Life Insurance and Why Choose It?

There is no payout if the plan ends before your fatality or you live past the plan term. You might be able to renew a term plan at expiry, however the premiums will be recalculated based on your age at the time of revival. Term life insurance policy is normally the the very least expensive life insurance policy readily available because it provides a survivor benefit for a limited time and doesn't have a cash worth element like irreversible insurance policy - Increasing term life insurance.

At age 50, the premium would climb to $67 a month. Term Life Insurance Rates thirty years old $18 $15 40 years of ages $28 $23 half a century old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for males and females in outstanding wellness. On the other hand, right here's a take a look at rates for a $100,000 whole life policy (which is a type of long-term plan, indicating it lasts your lifetime and includes money worth).

The decreased risk is one variable that allows insurance companies to bill reduced costs. Rate of interest prices, the financials of the insurance provider, and state guidelines can likewise affect premiums. As a whole, business frequently use better rates at the "breakpoint" coverage levels of $100,000, $250,000, $500,000, and $1,000,000. When you take into consideration the amount of coverage you can obtain for your premium bucks, term life insurance policy tends to be the least costly life insurance policy.

{kind=link}

Latest Posts

Final Expense Insurance Companies

Life Insurance Burial

Term Life Insurance Instant Online Quote